.png)

System credit and deposit growth

In this latest edition of Investor Compass, we talk about overall credit and deposit growth in FY23, performance of key operating indicators, and the evolving trends in the Banking space. So far CY23 has been fairly dynamic with inflation, both WPI & CPI, softening sharply, RBI changing its stance towards accommodation and pausing the rate hikes, credit growth remaining strong and asset quality across banks continuing to improve. Despite the strong run-up in the last few months, we continue to remain constructive on the sector.

System credit and deposit growth

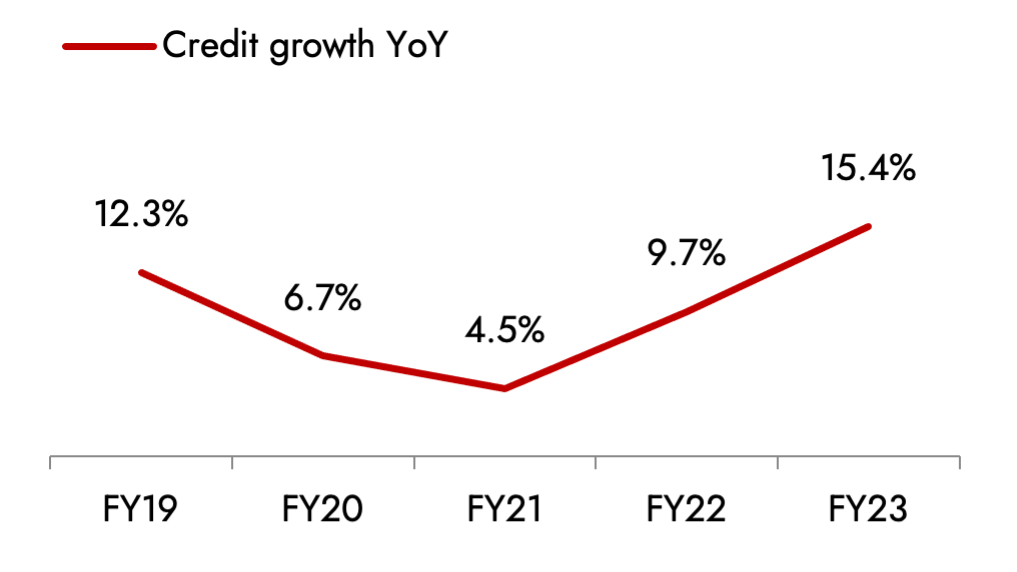

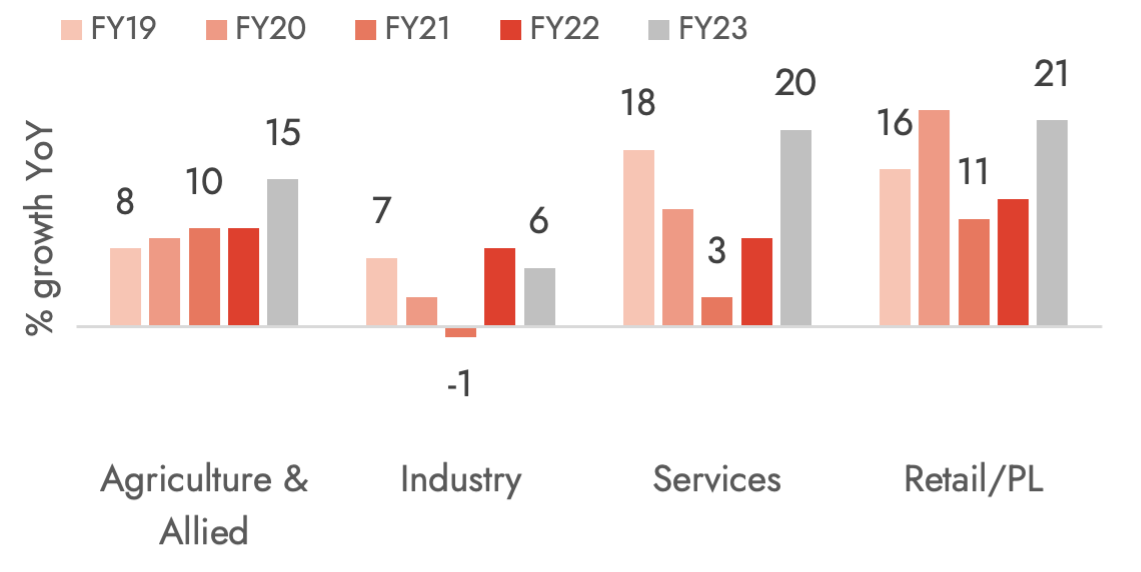

- Overall credit growth stayed healthy at 15.4% YoY in FY23, with accelerating trends seen in both, rural and urban regions. Credit growth has been relatively broad-based across segments (ref. Exhibit 2), supported by rather strong momentum in MSME, retail, and large corporate sectors.

- Within retail, while housing loan growth stood well at 15% YoY in FY23, unsecured credit experienced significant growth as personal loans and credit cards registered a growth of 25% and 31% YoY, respectively.

Chart 1: Revival of credit growth to mid-teens... Chart 2: Broad-Based credit growth…

Source: Ambit Asset Management, RBI database

- Private Banks benefited from their increased exposure to higher-yielding unsecured retail credit (credit cards, personal loans, MFI loans) and secured loans in housing, business banking, and SME segments. Focus on unsecured book has increased for HDFC Bank, Kotak Bank, Indusind Bank, Axis Bank, and IDFC First Bank.

- On the other hand, while corporate segment growth remained subdued for most banks, ICICI Bank delivered 21% YoY growth in its domestic corporate portfolio.

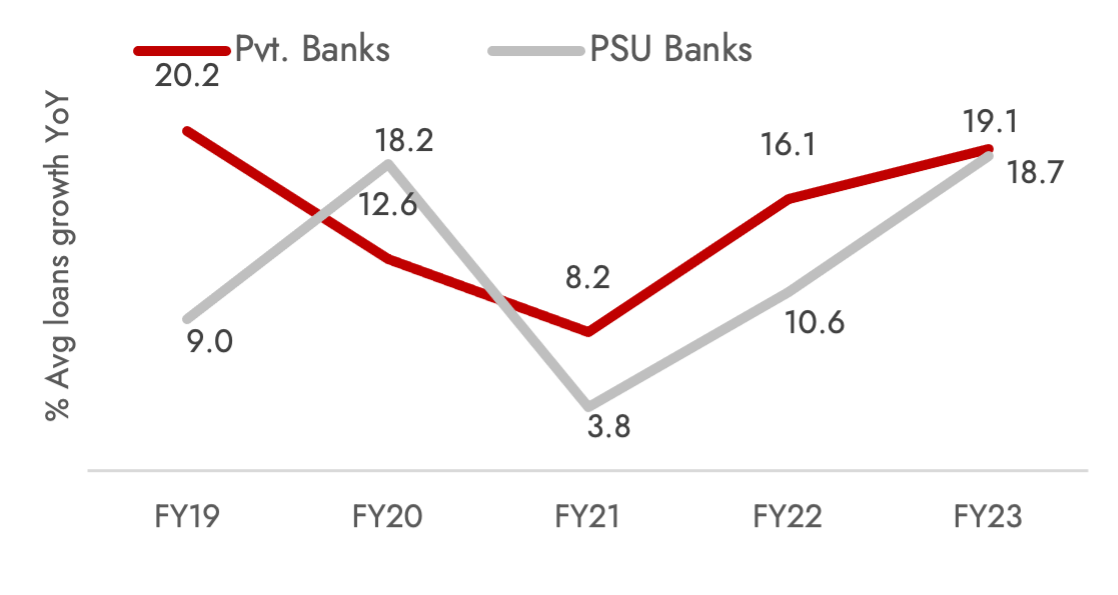

- PSU Banks focused on secured retail credit, MSME loans, and agricultural loans, delivering credit growth on par with the overall system growth, unlike the pre-COVID period. It is important to note that the growth gap between private banks & PSU banks has narrowed significantly (ref. Exhibit 3). International loan book growth continued to be a key growth driver for PSU banks.

Chart 3: Narrowing the gap between PVBs & PSBs Chart 4: Deposits growth lags advance growth

Source: Ambit Asset Management, RBI database

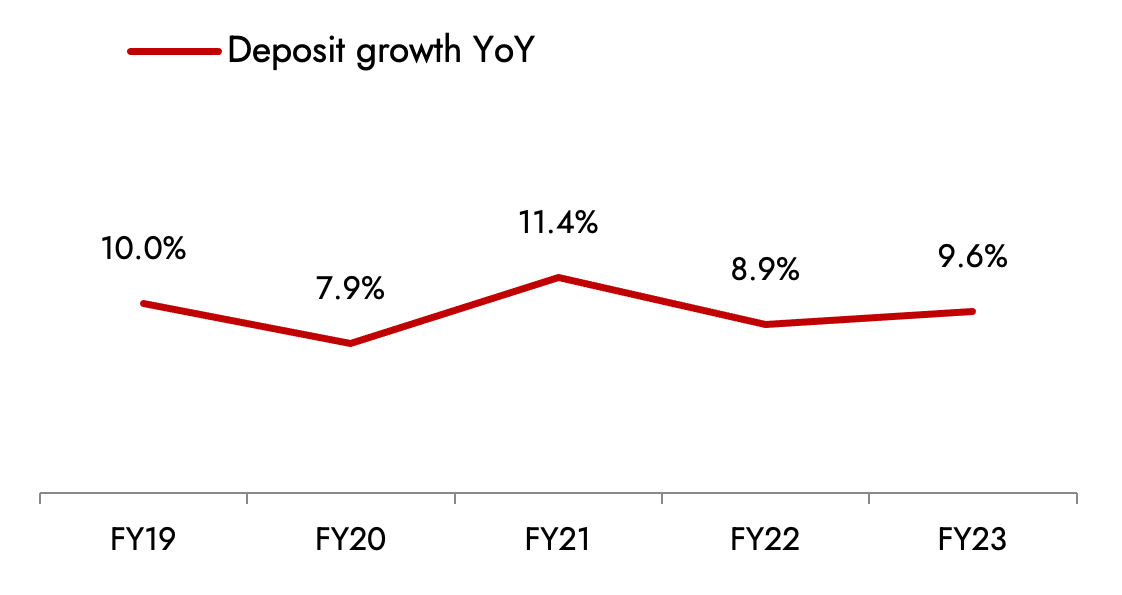

- Overall system deposit growth improved to ~10% (ref. Exhibit 4). It continued to lag system loan growth in FY23. CD ratio stood at 75.8%. Low deposit growth for banks is attributable to slow-paced savings deposit rate revisions made by banks despite the 250bps rise in repo rate. Withdrawal of INR2000 notes from circulation may improve deposit growth in the near term.

- CASA ratio across most banks moderated in FY23 (ref. Exhibit 5) owing to favourable term deposit rate revisions by banks which made FD (Term Deposits) more attractive, relatively. However, as an exception, Axis Bank saw CASA improvement of 215bps YoY on account of Citi book inclusion during FY23.

Chart 5: Moderation in CASA mix…

| CASA (%) | Q4FY23 | Q3FY23 | Q4FY22 | QoQ | YoY |

| Public Sector Banks | |||||

| SBI | 43.8 | 44.5 | 45.3 | -70bp | -150bp |

| Bank of Baroda | 42.3 | 41.6 | 44.2 | 70bp | 190bp |

| Private Sector Banks | |||||

| HDFC Bank | 44.4 | 44.0 | 48.2 | 40bp | -380bp |

| ICICI Bank | 45.8 | 45.4 | 48.7 | 40bp | -290bp |

| Axis Bank | 47.2 | 44.5 | 45.0 | 270bp | 220bp |

| Kotak Mahindra Bank | 52.8 | 53.3 | 60.7 | -50bp | -790bp |

| IndusInd Bank | 40.0 | 41.9 | 42.7 | -190bp | -270bp |

| Federal Bank | 32.7 | 34.2 | 36.9 | -150bp | -420bp |

| DCB Bank | 28.0 | 27.6 | 26.8 | 40bp | 120bp |

| AU SFB | 38.4 | 38.4 | 37.3 | 0bp | 110bp |

Source: Ambit Asset Management, Company

Going into FY24…

- Loan growth: Channel checks reveal a clear and aggressive focus from both, private and public sector banks, to expand their loan portfolios, especially in retail and unsecured lending segments.

- Based on RBI’s SCB (Scheduled Commercial Banks) fortnightly data releases and the current run-rate (Apr’23/May’23), system credit is expected to grow at a rate of ~3% QoQ (~15% YoY) for Q1FY24E, recording highest Q1 growth over the past 10 years, despite it being a slow period.

Some key trends being witnessed:

- Even though growth has started to slow down from 2QFY23 levels (~16-17%), the deceleration remains slow-paced.

- Retail demand in rural and semi-urban markets is showing signs of continued growth.

- Structural demand visibility, govt. support (reforms and subsidies) and healthier corporate balance sheets are likely to push capex up for the corporate sector.

- Improving economic activities and the requirement of working capital-linked products for MSMEs is expected to drive loan growth through NBFCs.

- Deposit growth: Although the gap between credit growth and deposit growth is narrowing, deposit mobilization by banks at competitive rates remains a key factor to monitor from a long-term perspective.

Some key trends being witnessed:

- Deposit mobilization by banks was skewed in the 1- 3 year bucker owing to their preference for shorter-term deposits to mitigate the impact of potential rate reversals on NIMs.

- Lags in interest rate revision of deposits indicate a likely increase in the cost of funds for banks as a very large share of term deposits is still below the card rate.

- Overall on the liquidity front, most private banks have LCR of ~123% while PSBs higher at ~150%, indicating PSBs are better placed to fund their credit book growth. The Indian banks have bonds worth Rs17trn in excess of regulatory requirements which adds to their ability to lend & support growth.

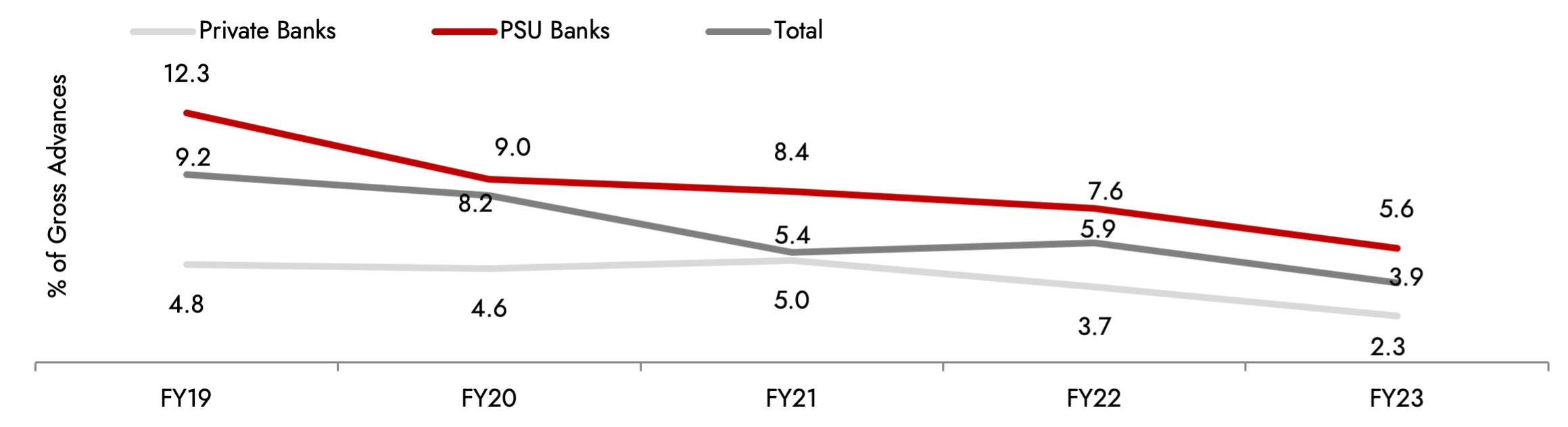

Overall asset quality improved; no longer a concern for banks

- Improved underwriting practices resulted in GNPA at a 7-year low & NNPA at a 10-year low. The banking system witnessed the best asset quality trend (recoveries > slippages) since 2016.

- During Q4FY23, the asset quality continued to improve as the GNPA ratio at the industry level declined by 66 bps QoQ to 3.9% (ref. Exhibit 6). Restructured book across banks continued to be on a declining trend.

- Going ahead, asset quality is unlikely to be a concern for most banks in the medium term, unless there is a sharp macroeconomic downturn.

- Expect incremental slippages to be low and recoveries/upgrades to stay strong, resulting in low credit costs in the near term. Some uncertainty may pertain around implementation of ECL (Expected Credit Loss) regime. However, we believe, it can be seen as a mere change in accounting treatment with no bearing on the banking system's performance fundamentally.

Exhibit 6: Improving asset quality on broad-based level…

Source: Ambit Asset Management, RBI database

Profitability: Return matrix to be maintained

- Margins: During FY23 most of the PVBs & PSBs witnessed flat to marginally positive trends on Net Interest Margins (NIMs). Yields inched up for most banks as they saw a modest pass-through of the higher benchmark interest rates after the RBI hiked repo rates.

- Banks with a higher External benchmark linked rate (EBLR) rated loan mix witnessed stronger growth upon immediate loan re-pricing.

Exhibit 7: Higher floating book results in faster NIMs expansion…

| CASA (%) | Q4FY23 | Q3FY23 | Q4FY22 | QoQ | YoY |

| Public Sector Banks | |||||

| SBI | 3.4 | 3.3 | 3.0 | 10bp | 40bp |

| Bank of Baroda | 3.5 | 3.5 | 3.1 | 0bp | 40bp |

| Private Sector Banks | |||||

| HDFC Bank | 4.2 | 4.3 | 3.9 | -10bp | 30bp |

| ICICI Bank | 4.8 | 4.7 | 3.9 | 10bp | 90bp |

| Axis Bank | 3.9 | 4.1 | 3.3 | -20bp | 60bp |

| Kotak Mahindra Bank | 5.8 | 5.5 | 4.8 | 30bp | 100bp |

| IndusInd Bank | 4.1 | 4.1 | 4.0 | 0bp | 10bp |

| Federal Bank | 3.2 | 3.5 | 3.1 | -30bp | 10bp |

| DCB Bank | 4.0 | 3.9 | 3.7 | 10bp | 30bp |

| AU SFB | 5.8 | 6.0 | 6.0 | -20bp | -20bp |

Source: Ambit Asset Management, Company

- Going ahead, we expect banks with a higher share of Marginal Cost of Funds based Lending Rate (MCLR) linked loans (ref. Exhibit 7) to witness a higher amount of upward re-pricing of advances. However, re-pricing of deposits will gather pace slowly.

- For most banks, the Cost of funds transmission is still not complete, while lending yields have limited room for improvement, thereby limiting the scope of growth for the net interest income.

- We expect margins to have peaked out and remain watchful of:

- Any disruption to the pace of deposit mobilization, thereby impacting NIMs.

- Any abrupt and sharp reversal of interest rates led by external conditions will have a negative impact on NII growth.

Exhibit 8: Higher floating book results into faster margin expansion…

| Fixed Rate | EBLR | MCLR | Others | |

| Public Sector Banks | ||||

| SBI | 25% | 24% | 41% | 10% |

| Bank of Baroda | 7% | 30% | 50% | 13% |

| Private Sector Banks | ||||

| HDFC Bank | 45% | 40% | 15% | |

| ICICI Bank | 30% | 45% | 20% | 5% |

| Axis Bank | 32% | 41% | 20% | 7% |

| Kotak Mahindra Bank | 30% | 57% | 13% | |

| IndusInd Bank | 51% | 49% | ||

| Federal Bank | 25% | 50% | 15% | |

| AU SFB | 66% | |||

Source: Ambit Asset Management, RBI database

- Operating Profitability: In FY23, banks reported healthy earning growth, led by strong operating profit and declining provisions.

- Going forward, given the branch expansion and technology investment plans undertaken by most banks, it is clear that the opex will remain at elevated levels across banks but lower credit costs (assuming there is no higher provision for ECL) should ensure sustenance of RoEs at the current levels.

Outlook:

- We expect the current convergence theme in terms of loan growth between PVBs & PSUs to continue leading to higher competitive intensity.

- We expect deposit growth to accelerate from here in the medium term, supported by improved real deposit rates and normalization of CASA deposits. This coupled with a loan growth of 13-14% should drive strong overall performance for banks.

- From a macro perspective, while we expect a likely moderation in working capital demand as the spreads between WPI & CPI have moved from 880bs in May’22 to -780bps in May’23, we expect strong acceleration in capex by Centre, State & Corporates in FY24.

- For banks, while we expect NIMs to have peaked, operating leverage and lower credit costs should support RoEs and thereby the valuations.

Valuation (portfolio companies):

- HDFC Bank: Post-merger of Housing Development Finance Corporation with HDFC Bank, the bank will have the second largest branch network in the country which will further add value to it’s strong deposit franchise. Especially so, as balance sheet growth instead of margins will become key in FY24. We believe HDFC Bank is strongly footed to deliver quality performance. The stock trades at 2x FY25E P/B.

- ICICI Bank: The franchise is well-positioned to maintain its margins and deliver consistent loan growth, even in the expected moderation. Coupled with strong deposit franchises, and high-tech infrastructure, the bank has key levers in place to outperform peers. The stock trades at 2.1x FY25E P/B.

- Axis Bank: Amongst the banks, we believe Axis Bank is well positioned and showing signs of RoA re-rating upon complete integration of Citi Bank’s portfolio. Although there persists pressure on opex from the merger and on NIMs from higher CoF, the stock trades at 1.6x PB FY25E at a discount against peers, making the risk-reward attractive.

- Federal Bank: Management’s guidance of high-teen loan growth, FY24E NIMs at 3.3-3.35%, peaking out of CoF as 80% of deposits have been repriced reinstates our confidence in the franchise to have front-loaded expected risks and readied itself to deliver performance. The stock trades 0.9x FY25E BV.

- DCB Bank: We have faith in DCB’s core focus on a high proportion of secured lending to high-yielding self-employed customers, the ability to maintain a stable liability mix, maintain strong profitability with adequate cost controls. The stock currently trades at 0.7x FY25E BV.

- AU SFB: We believe the management implemented effective tech investment strategies and the bank will soon benefit from them as the operating leverage plays out. The bank enjoys margin comfort due to incremental high-yield lending despite the rise in deposit rates. Top management’s continuity plan further builds our confidence in the franchise. The stock currently trades at 3.5x FY25E BV.

Exhibit 9: Valuation of portfolio companies…

|

Particulars |

CMP |

RoA (%) |

RoE (%) |

P/BV |

||||||

|

|

|

FY23 |

FY24E |

FY25E |

FY23 |

FY24E |

FY25E |

FY23 |

FY24E |

FY25E |

|

HDFC Bank |

1648 |

2.0 |

1.9 |

1.9 |

17.0 |

17.8 |

16.3 |

2.9 |

2.4 |

2.0 |

|

ICICI Bank |

944 |

2.2 |

2.1 |

2.1 |

17.2 |

16.9 |

16.8 |

2.9 |

2.5 |

2.1 |

|

Axis Bank |

953 |

0.8 |

1.7 |

1.7 |

8.0 |

16.9 |

16.2 |

2.3 |

1.8 |

1.5 |

|

DCB Bank |

127 |

1.0 |

1.0 |

1.0 |

10.8 |

12.0 |

12.2 |

0.9 |

0.8 |

0.7 |

|

Federal Bank |

135 |

1.3 |

1.2 |

1.2 |

14.9 |

13.6 |

14.1 |

1.3 |

1.2 |

1.0 |

|

AU SFB |

763 |

1.8 |

1.7 |

1.7 |

15.4 |

14.2 |

15.1 |

4.6 |

4.1 |

3.5 |

*CMP as on 11/07/23

For any queries, please contact:

Umang Shah - Phone: +91 22 6623 3281, Email - aiapms@ambit.co. Registered Address: Ambit Investment Advisors Private Limited - Ambit House, 449, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Corporate Address: Ambit Investment Advisors Private Limited - 2103/2104, 21st Floor, One Lodha Place, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Risk Disclosure & Disclaimer

Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with the Securities and Exchange Board of India vide registration number INP000005059.

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.